Applying the Poisson Distribution in Financial Risk Management

Introduction

As a current master's student in Financial Engineering, I recently had the opportunity to explore the Poisson Distribution law and proof in my probability and statistics class. This statistical tool, which models the occurrence of rare events, piqued my interest due to its potential applications in finance—a field where understanding and predicting such events is crucial for risk management. I wanted to see how the Poisson Distribution could be applied in real-world financial scenarios, given its relevance to modeling rare but impactful events like loan defaults or stock market crashes.

The Poisson Distribution

The Poisson Distribution is a discrete probability distribution that models the number of events occurring in a fixed interval of time or space if these events occur with a known constant mean rate and independently of the time since the last event. It's particularly useful for predicting rare events, making it a valuable tool in financial risk assessment.

Applications in Financial Risk Management

In finance, the Poisson Distribution can be applied to model various rare events:

Loan Defaults: With the U.S. government planning to resume collections on defaulted student loans in 2025, understanding the likelihood of loan defaults is crucial. The Poisson Distribution can help financial institutions assess potential losses and adjust their risk management strategies accordingly.

Stock Market Crashes: Given the current volatility in the stock market, with concerns about inflation and geopolitical tensions affecting market stability, the Poisson Distribution can be used to model the risk of rare but significant market downturns.

Corporate Defaults: Recent data shows an increase in corporate defaults across various sectors, highlighting the importance of using statistical models like the Poisson Distribution to predict and manage these risks.

Benefits and Limitations

The Poisson Distribution offers several benefits in financial modeling, including simplicity and ease of interpretation. However, it assumes a constant mean rate of events, which might not always reflect real-world conditions where rates can fluctuate over time.

Conclusion

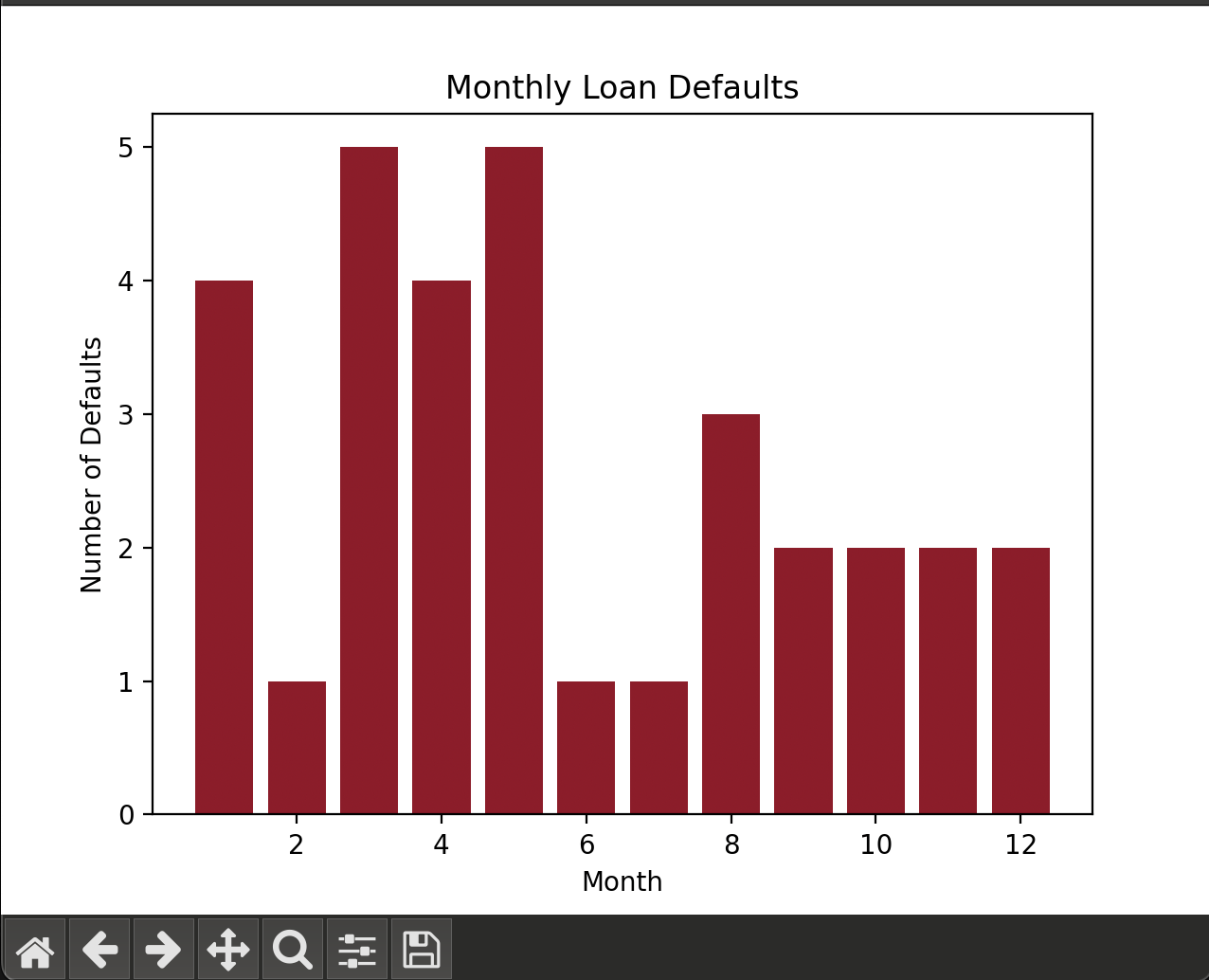

In conclusion, the Poisson Distribution provides a powerful framework for modeling rare events in finance, enhancing risk management capabilities. For those interested in seeing how this concept is applied in practice, refer to my project on Poisson Loan Default Modeling, available on my GitHub (see below for program output). This project demonstrates how to simulate loan defaults using the Poisson Distribution and calculate potential losses, providing a simple example of its application in financial risk management.

References

Understanding Poisson Distribution in Simple Terms

Finance Tutoring, 2025.

https://www.finance-tutoring.fr/understanding-poisson-distribution-in-simple-terms/?mobile=1Rare events: Handling Rare Events using the Poisson Distribution

Faster Capital, 2024.

https://fastercapital.com/content/Rare-events--Handling-Rare-Events-using-the-Poisson-Distribution.htmlThe U.S. Speculative-Grade Corporate Default Rate Could Fall To...

S&P Global Ratings, 2025.

https://www.spglobal.com/ratings/en/research/articles/250220-default-transition-and-recovery-the-u-s-speculative-grade-corporate-default-rate-could-fall-to-3-5-by-dec-13420343Will the Stock Market Crash in 2025?

U.S. News & World Report, 2025.

https://money.usnews.com/investing/articles/will-the-stock-market-crash-risk-factors